For those that didn’t enjoy the last few weeks of the tour through the price drivers of property prices, fear not: today is a new subject. We are

going to look at the current interest rates on offer – fixed and variable – increase your mortgage mortality rate and bury it.

Most of you already have mortgages through us now.

As I always harp on about, they never should be set and forget bills to pay.

Although the benefits of saving money can seem immaterial repayment by repayment, if managed well you will be (mortgage) free much sooner than many realise.

Let’s cover two key areas today.

I can go into more over the next few weeks if your feedback shows you want it, but I'll only push my barrow so much while I have your interest (last pun),

promise. Ok, second last: A new client asked me this week if I was vegetarian. I thought it was an odd question as I had never met herbivore.

Humph.

Ok, let’s get on with it:

Let’s look at fixed rates vs current variable rates and how you might think about it. Before doing a

straight comparison there are a few general rules on fixed rates, that you will know but let’s recap:

In General:

Why have a fixed rate?

Lock in your loans repayments for the fixed rate period so you know exactly what you are in for, on one your main expenses.

Often cheaper than current variable rates. This relationship varies and I won’t get too technical although right now they are materially lower.

Risk management – you don’t have to be concerned about economic issues if you are on a fixed rate – you are effectively sheltered if there is a tumult on the markets and rates

unexpectedly rise.

Why not?

You do not plan to hold the property as long as the fixed rate period.

You will

regret fixing if rates fall further – this is quite a common emotion and it is important to remember why you fixed it at the time.

Inflexible if you want to refinance, get equity out, or restructure your portfolio.

Generally, more restrictive than variable – no offset account, limits on extra

repayments.

The rate often defaults to a higher rate after the fixed rate period expires.

As many of you know from the conversations and refinancing, we have been doing over the last few months, in most cases we can solve for points 4. and 5. and the 1-3 require consideration by you.

Often for those with investment properties, a good strategy can be to consider fixing the investment loan and keep your owner-occupied variable, but again we discuss all this with you and can solve for points 3-5 through lender choice and account set up.

Let’s get to the juicy stuff. RATES.

I put these charts together based on existing rates with lenders I am prepared to recommend. Rate is important but like most things, it is not a one-dimensional consideration.

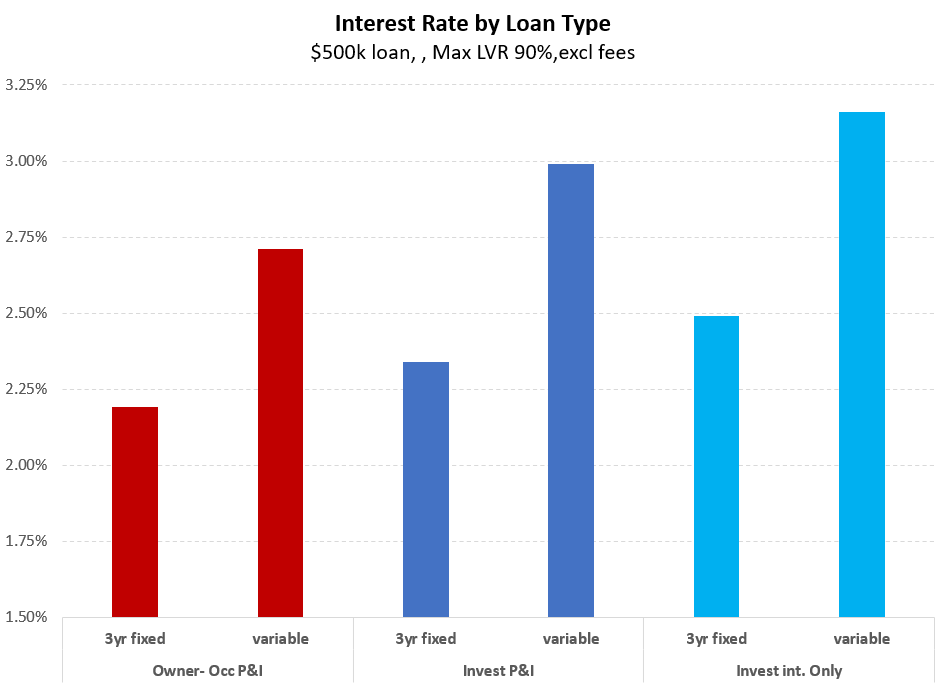

I compiled this chart based on Friday’s rates for a new $500k loan.

A few things are worth highlighting:

The fixed rates on offer are well below what many think the variable rate can drop to, especially for investment properties.

There is now little if any difference in rates at an 80% or 90% Loan to Value Ratio (LVR). In this environment, I conclude that lenders are more concerned about income security than property price risk itself (quite a message here!)

The premium of investment property and owner-occupied rates has decreased. This was close to 1%. about two years ago and now down to 0.25%

Additionally, the premium of interest-only to P&I repayments on an investment property is as low as 0.2%. Two years ago, this was up to 0.9%

What does this really mean?

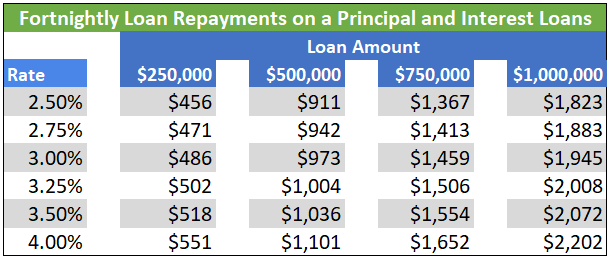

This table shows the fortnightly repayments for various rates and loan sizes for a 30yr P&I loan:

You can draw your own conclusion whether this is material enough but lets now return to the earlier point and reducing the expected life of the mortgage (mortality)

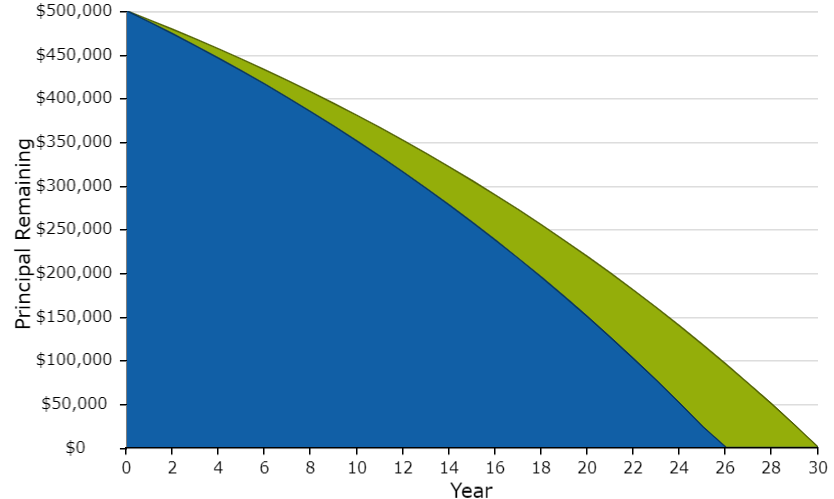

Mortgage Mortality.

Like one of my favourite books, The Slight Edge, 9over highlights; small things don’t make much difference in the short term, but in the long

term they do. E.g. missing a day’s exercise won’t matter too much, missing a month will, and missing a year, well…

Using the repayment table above, if you are on a 3.5% rate for a 30 year $500,000 loan and it was reduced to 3%, your fortnightly repayments would be $97 less. Yes, it's $6.95 per day - nice but hardly life-changing.

However, if you did the "right thing" and kept your repayments the same (so make additional repayments above the minimum each fortnight) this would reduce the mortgage life by 4.1 years.

4.1 years of mortgage free life and not a sweat raised, or burger missed.